The IRS has finally announced adjustments to 2022 contribution limits on various tax-advantaged health and dependent care spending accounts, retirement plans, and other employee benefits such as adoption assistance and transportation benefits. Many of these contribution limits, though not all, are indexed to cost-of-living adjustments.

The IRS has finally announced adjustments to 2022 contribution limits on various tax-advantaged health and dependent care spending accounts, retirement plans, and other employee benefits such as adoption assistance and transportation benefits. Many of these contribution limits, though not all, are indexed to cost-of-living adjustments.

Together, these combined announcements by the IRS detail 2022 adjusted limits to the amounts employees can tuck away pretax into Flexible Spending Accounts (FSAs), Health Savings Accounts (HSAs), transportation benefits, and retirement plans such as 401(k)s.

While IRS limits for HSAs and HDHPs are required, by law, to be announced by June 1st, limits for these other pretax savings vehicles always seem to come so late in the year that many employers have already completed their employee benefits open enrollments.

Employers who have already completed open enrollment for 2022 have two choices when it comes to communicating these updates; 1) they can do nothing, since there isn't an obligation to make the maximum election amounts available to employees, or 2) they can reopen the enrollment process and let employees who want to increase their elections do so before December 31st, for calendar year plans.

What follows is a summary of the new IRS limits;

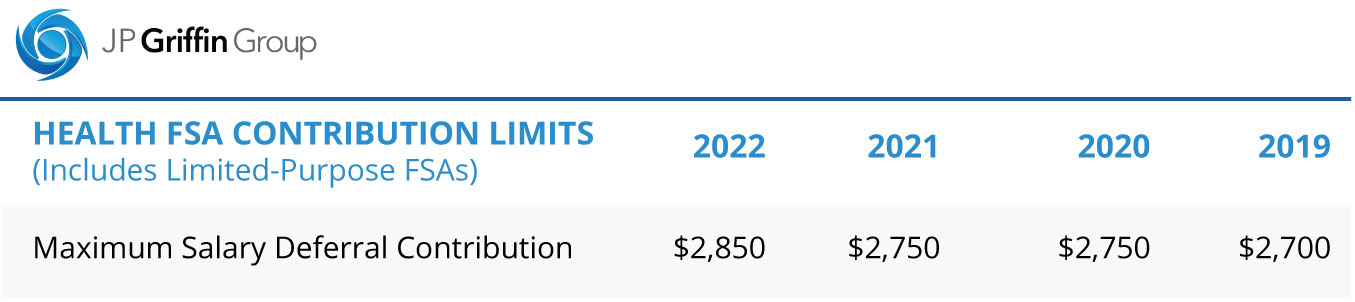

Health Care FSA Limits Increase for 2022

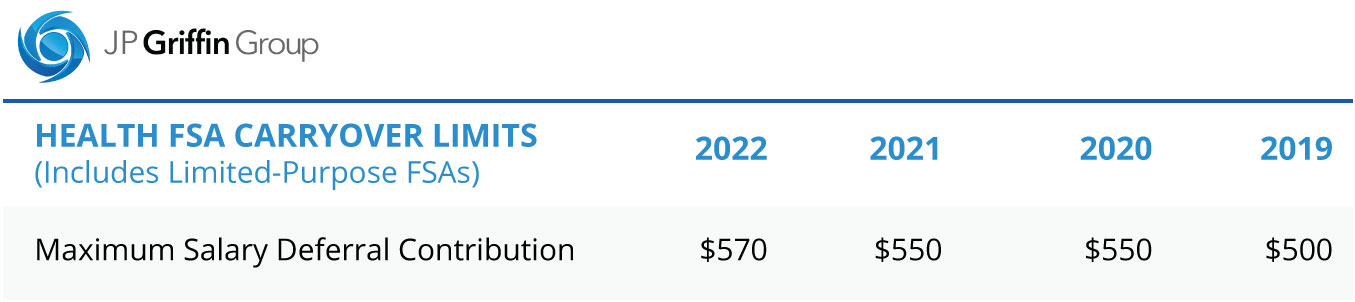

Employees can deposit an incremental $100 into their health care FSAs in 2022. And if an employer's plan allows for carrying over unused health care FSA funds, the maximum carryover amount has also risen, up $20 from $550 in 2021, to $570 in 2022.

These new limits also apply to limited-purpose FSAs which are used with HSAs to provide employees with tax-advantaged funds to pay for qualified dental and vision care services.

While FSA funds not spent within the plan year often times come with a two-and-a-half-month grace period to spend remaining balances, the Consolidated Appropriations Act of 2021 granted employers additional leeway in terms of how they can allow employees to carry over unused balances. These include the ability to carry over unlimited unspent funds from both 2020 and 2021 into 2022. Additional options exist for employers who choose to grant carry-over extensions, but employers cannot blend grace periods and carry-overs.

It's also worth noting that any amount that rolls over into the new plan year does not affect the maximum limit that employees can contribute.

FSA Employer Contribution Limits for 2022

Employers can also provide health care FSA contributions, in addition to the amount that employees can elect. In fact, employees can elect up to the IRS limit and still receive this employer contribution in addition to those amounts.

These employer contributions to a health care FSA are based on how much the employee contributes:

- An employer may match up to $500, regardless of whether or not the employee contributes to a health FSA themselves.

- Above $500, employers may only make a dollar-for-dollar match to the employee’s contribution.

In general, however, employer contributions should not exceed $500 per plan year for a health care FSA to maintain excepted benefit status, which avoids making it subject to certain ACA and HIPAA requirements.

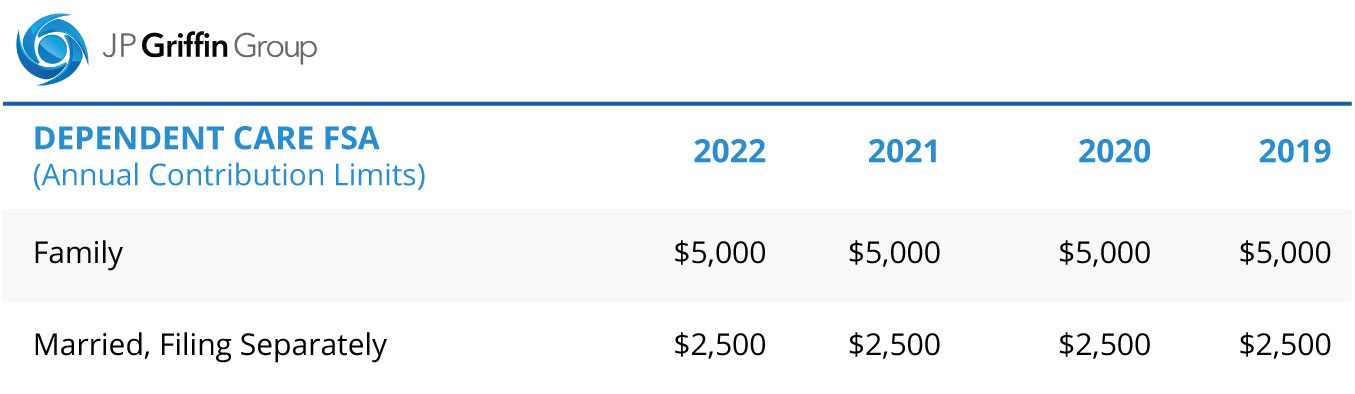

Dependent Care FSA Limits Stay Flat For 2022

Unlike the health care FSA, which is indexed to cost-of-living adjustments, the dependent care FSA maximum is set by statute. For 2022, it remains $5,000 a year for individuals or married couples filing jointly, or $2,500 for a married person filing separately.

To be clear, married couples have a combined $5,000 limit, even if each has access to a separate dependent care FSA through his or her employer.

Employers can also choose to contribute to employees' dependent care FSAs. However, unlike with a health care FSA, the combined employer and employee contributions to a dependent care FSA cannot exceed the IRS limits noted here.

Eldercare may be eligible for reimbursement with a dependent care FSA if the adult lives with the FSA holder at least 8 hours of the day and is claimed as a dependent on the FSA holder's federal tax return.

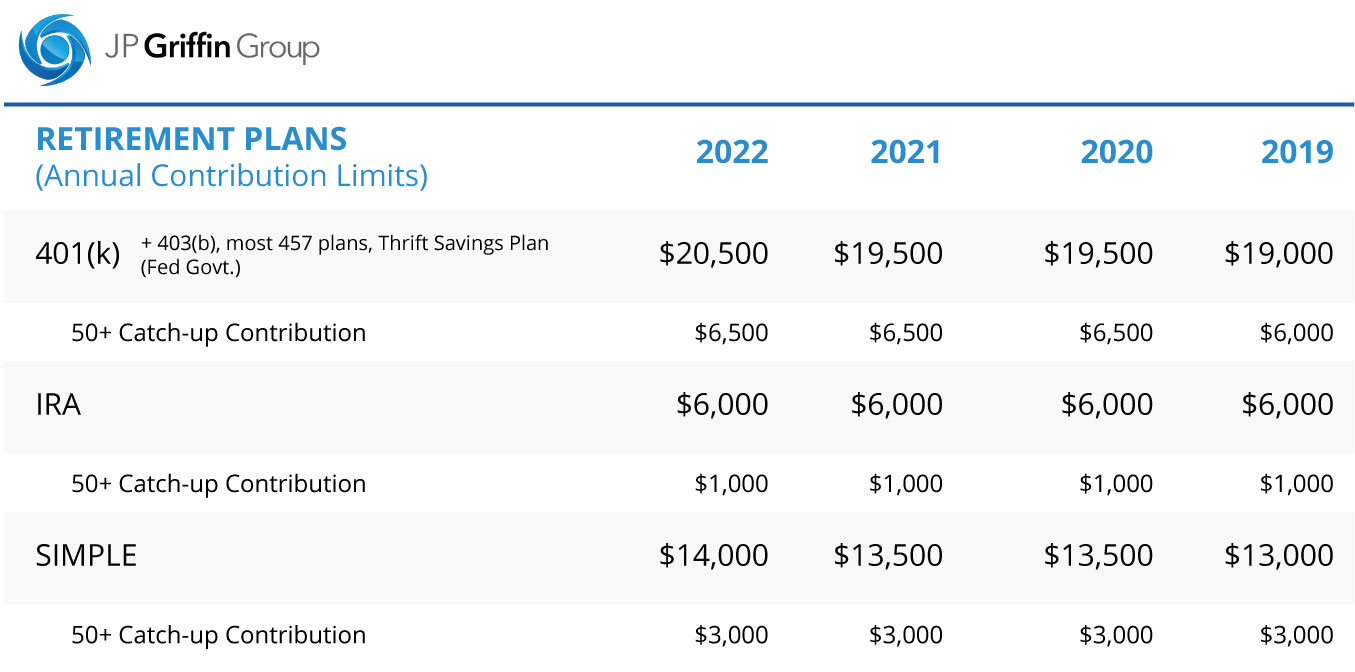

2022 Retirement Plan Limits Increase

The IRS also increased the amount employees can contribute to 401(k) plans, raising the contribution cap to $20,500 while the catch-up contribution remains unchanged at $6,000.

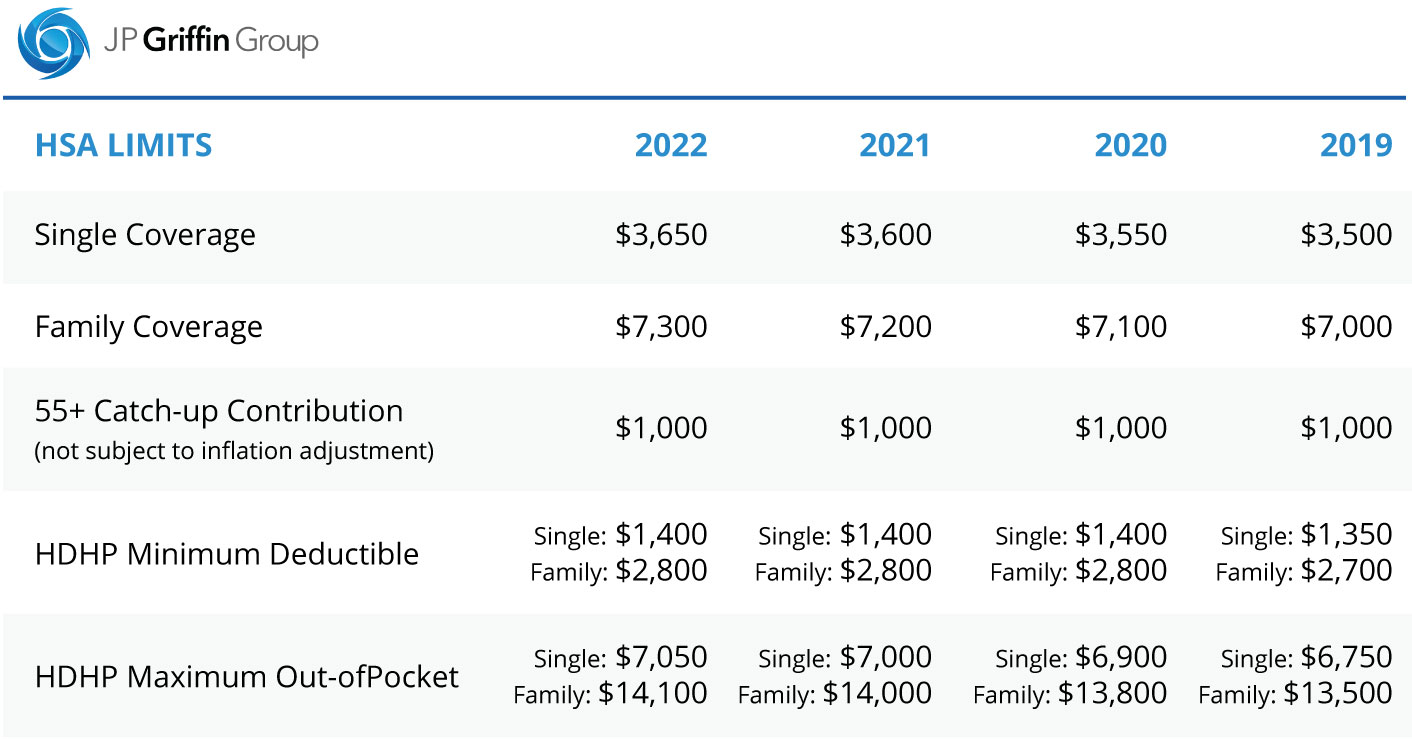

HSA & HDHP Limits Increase for 2022

Earlier this year the IRS also announced changes in limits on Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs) for 2022. These limits include:

- The maximum HSA contribution limit;

- The minimum deductible amount for HDHPs; and

- The maximum out-of-pocket expense limit for HDHPs.

These limits vary based on whether an individual has self-only or family coverage under an HDHP.

- Eligible individuals with self-only HDHP coverage will be able to contribute $3,650 to their HSAs for 2022, up from $3,600 for 2021.

- Eligible individuals with family HDHP coverage will be able to contribute $7,300 to their HSAs for 2022, up from $7,200 for 2021.

- Individuals who are age 55 or older are permitted to make an additional $1,000 “catch-up” contribution to their HSAs.

The minimum deductible amount for HDHPs remains the same for 2022 plan years ($1,400 for self-only coverage and $2,800 for family coverage). However, the HDHP maximum out-of-pocket expense limit increases to $7,050 for self-only coverage and $14,100 for family coverage.

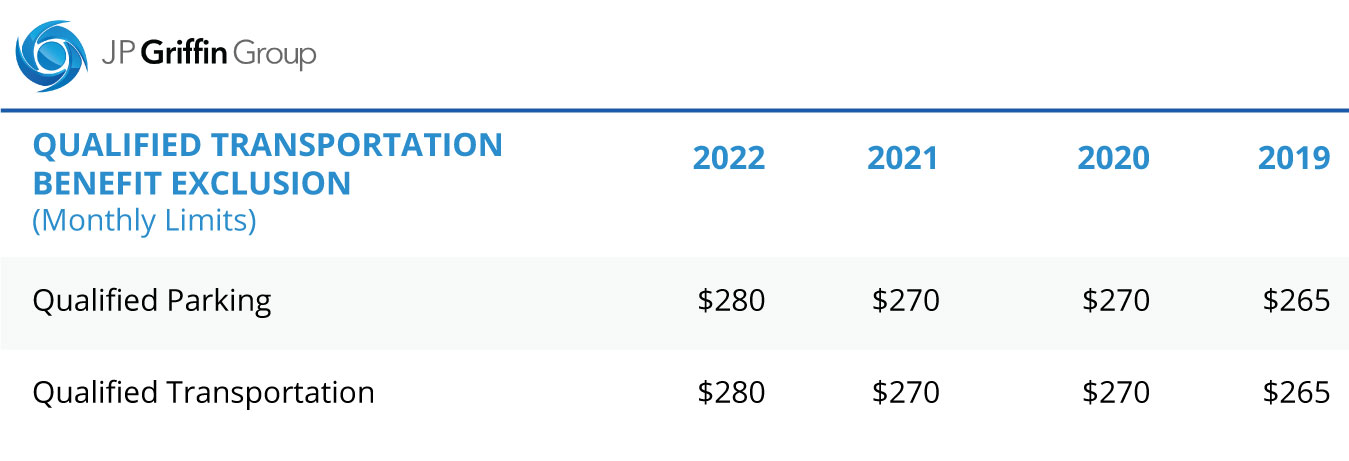

Transportation Fringe Benefits Rise for 2022

The monthly limit on expenses for work-related mass transit expenses (for example, bus and train fare), as well as parking, rises to $280 for 2022, which is $10 more than in 2021.

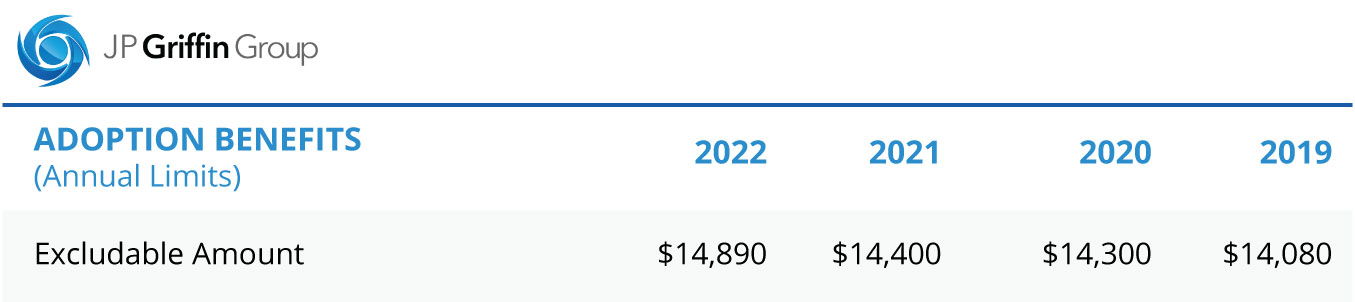

Adoption Assistance Increases for 2022

For 2022, the maximum amount of an employer subsidy for qualified child-adoption expenses that can be excluded from an employee's gross income will be $14,890, up from $14,400 for 2021.

Qualified Small Employer HRAs for 2022

For tax year 2022, to qualify as a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA), the total amount of payments and reimbursements by employers for any year cannot exceed $5,450 for individual coverage or $11,050 for family coverage.

Educating Employees On The Changes

It’s important to advise employees considering making changes to their contribution elections that changes to most (but not all) of these savings vehicles can only be made during your company’s annual open enrollment period, or after a Qualified Life Event (QLE).

It's also important to remind them that unlike unspent HSA funds, which roll-over, FSA funds are "use-it-or-lost-it" and expire at the end of the year. It should also be stressed that while the IRS allowed employees to make mid-year adjustments to their FSA contributions these past two years, that flexibility will no longer exist in 2022.

For employees contributing to an FSA, it's also a good idea to remind them that these tax-deferred funds will be available, in full, at the start of the plan year, even though contribution amounts will be equally deducted from their pretax earnings each pay period.

If you have any questions about this year’s IRS limits as they relate to these or other employee benefits, contact us right away.